The UK housing market continued to lose steam in September, as high interest rates and low consumer confidence weighed on demand. However, the rate of decline eased slightly compared to the previous month, according to the latest data from Halifax.

Halifax HPI shows 0.4% monthly drop

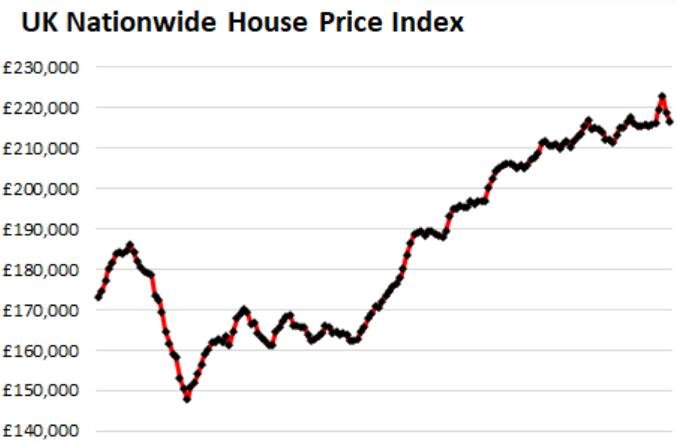

Halifax, the UK’s largest mortgage lender, reported that the average house price fell by 0.4% in September, following a 1.8% drop in August. This was the sixth consecutive monthly fall, but the smallest since March this year.

The annual rate of change also moderated slightly, from -4.5% in August to -4.7% in September. The average home now costs £278,601, down by around £1,200 since last month and by £14,000 since the peak in August 2020.

However, house prices are still £39,400 higher than in March 2020, before the pandemic triggered a surge in demand for more spacious and rural properties.

Interest rates and affordability remain key factors

The main reason for the cooling of the housing market is the sharp rise in interest rates since December 2020, when the Bank of England started to tighten monetary policy to combat inflation. The Bank has raised its base rate 14 times since then, reaching 5.25% in August.

This has pushed up the cost of borrowing for homebuyers, especially those with high loan-to-value ratios or variable-rate mortgages. The average rate on a two-year fixed-rate mortgage has risen to about 6.67%, according to Moneyfacts.

Kim Kinnaird, director of Halifax Mortgages, said that higher interest rates have reduced affordability and deterred prospective buyers from entering the market.

“Market activity levels slowed during August, and while there is always a seasonality effect at this time of year, it also isn’t surprising given the pace of mortgage rate increases over June and July,” she said.

“While these did ease last month, rates remain much higher compared to recent years. This may well have prompted prospective buyers to defer transactions in the hope of some stability, and greater clarity on the future direction of rates in the coming months.”

She added that the market will continue to rebalance until it finds an equilibrium where buyers are comfortable with mortgage costs in a higher range than seen over the previous 15 years.

Regional variations and outlook

The Halifax data also showed that house prices fell in every region of the UK in the third quarter of 2023, compared to the same period last year. The south-west of England saw the biggest drop, at 6.3%, followed by London and the south-east, both at 5.9%.

The smallest declines were recorded in Scotland and Northern Ireland, both at 3.2%, and Wales at 3.4%.

Kinnaird said that the south of England has seen more downward pressure on prices due to its higher exposure to interest rate changes and lower income growth.

However, she also noted that income growth has remained strong overall, which has improved affordability for first-time buyers. The house price-to-income ratio for this group has fallen from 5.8 in June 2020 to 5.1 in September 2021.

She also said that the Bank’s decision to hold interest rates at 5.25% in September may have helped to lower longer-term interest rates, which could ease mortgage costs in the future.

However, she warned that interest rates are unlikely to return to their record low levels of the pre-pandemic period anytime soon, as inflation remains well above the Bank’s 2% target.

“Overall, these factors are likely to keep mortgage rates elevated in comparison to recent years, constraining buyer demand and putting downward pressure on house prices into next year,” she said.